What can PMC bank do for its stressed depositors after hiding defaulter HDIL's NPAs for so long?

Total Views |

By Siddhi Somani -

Banking has always been a nerve system of the country's financial structure. But in the recent times, the paradigm change in the landscapes of banking has posed significant challenges to the said nerve system as well as the regulators. Unfolding the PMC bank scam, the concerned authorities have finally moved up taking action against the wrong-doings, saving a corner of justice for the depositors.

Compliance risk being of legal or regulatory sanctions, material financial loss or loss to reputation, the Punjab nd Maharashtra Cooperative Bank, is said it suffered as a result of its failure to comply with laws, regulations, rules, related self-regulatory organization standards and codes of conduct applicable to its banking activities.

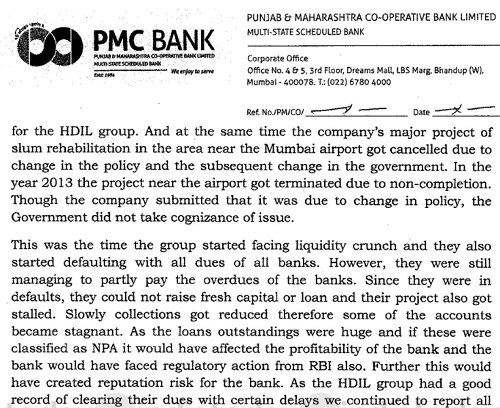

The crisis at PMC surfaced a week after it noted huge losses owing to loans that had gone sour. The Mumbai Police filed a First Information Report against the promoters of Housing Development and Infrastructure Ltd, a listed real estate development company's Sarang Wadhawan and Rakesh Kumar Wadhawan and PMC's former managing director Joseph Thomas, for allegedly colluding to cheat the bank of up to Rs. 4,300 crore.

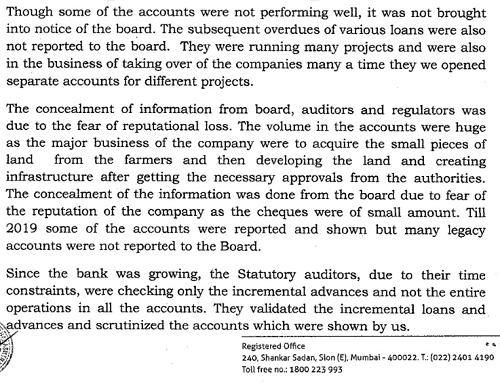

PMC had earlier not mentioned the loan default by HDIL in its annual report and continued to give loans despite the company being taken for insolvency. PMC's exposure to HDIL nearly stands 73 per cent of its total loan book size of Rs. 8,880 crore as of September 19. Further, despite HDIL not repaying, the bank officials did not classify the loans as non-performing advances and intentionally hid the information from the RBI.

With this the depositors at cooperative banks are now in a relatively higher risk zone as the supervision and administration of these entities falls under state governments and the central bank. The central bank cannot take any action against the banks unilaterally but can suggest a plan to the state government which has the ultimate authority to decide if the bank should continue operations or be shut down.

The Reserve Bank of India on September 24 imposed a six month ban on the Mumbai based PMC bank on the charges of irregularities, further issuing a special guideline to monitior all the transactions of the said bank affecting the depositors at large. With this, the saving, current, fixed deposit account holders were permitted to withdraw only Rs 1000 within six months but eventually could deposit the amount they wanted to secure.

Further, making it clear that the banking license of the PMC Bank was not cancelled and that it could continue its operations under the set restrictions, the apex bank stepped up to reduce the hardships of the depositors, allowing them to withdraw Rs 10000 within six months. But the actual reason behind the RBI's move in case of this particular cooperative bank remained under the carpets unless it was reported in detail to the police.

With this it would have been appreciable if the RBI communicated with depositors regarding when would they get access to their money? How did the bank fraud go unnoticed for a decade? Which other bank fraud had been missed while napping over the last 10 years?

Demonstrating a good compliance culture is the most significant stance to be undertaken by any bank, be it a commercial, cooperative,national, rural, any of it! This leads to maintain their reputation and win the trust of customers, investors and regulators. Such culture is important for banks also to avoid poor conduct and loss of trust. Now trapped in a financial conspiracy, PMC bank needs to take suggestive quick stands, not only for the depositors but for its self survival too!